03 Jul Well Within Your Rights – asking your plumber for details of his insurance

IMPORTANT CLAIMS HANDLING UPDATE

Any blog post in the Metropolis Solutions Blog Archive that includes any direct or indirect reference to insurance claims handling of any nature whatsoever, including any reference to existing and/or potential claims, was posted prior to 01.07.21, is for general information only and may also no longer be applicable due to recent changes in Federal Financial Services laws concerning claims handling. Please note that Metropolis does not hold an Australian Financial Services (AFS) Licence for claims handling and therefore qualified expert assistance on any insurance related matter, including Victorian Plumbers Warranty, should now be sought from a suitable lawyer or other expert holding an AFS claims handling licence. Metropolis Solutions can still consult on insurance claims handling matters, but only in the instance where we are directly engaged to do so by your authorised legal representative.

When you engage the services of a licenced plumber, do you ever consider what could go wrong? The answer is PLENTY of things can and do go drastically wrong every single day! Consider that plumber’s deal primarily in the transport of fluid in, out, beneath and on top of your home or your work place. Murphy’s Law was most probably written for plumbers and their apprentices (bless them all, it’s often not an easy job!).

During the course of our investigations into defective works carried out by plumbers and the resultant damages that ensue, a common theme has emerged – it’s bloody hard to get the insurance details of the plumber after the fact. The bad plumbers can have insurance policy excesses up to or beyond $10,000 and depending on how many claims they can have, any further claims on their policy may spell the end of their licence if they can no longer secure insurance.

The current situation is that whilst the plumber’s name and licence number must be referenced on the Compliance Certificate, their mandatory insurance details are held securely by the Victorian Building Authority (VBA). Recently, changes to VBA policy have resulted in these insurance details being firmly hidden behind the Freedom of Information curtain which means that even if a consumer has clearly been the victim of defective work and/or significant resultant damage, access to the all-important insurance details is severely restricted and in fact their release can even be vetoed by the plumber on ‘privacy’ grounds – holding up any progress for months if not years.

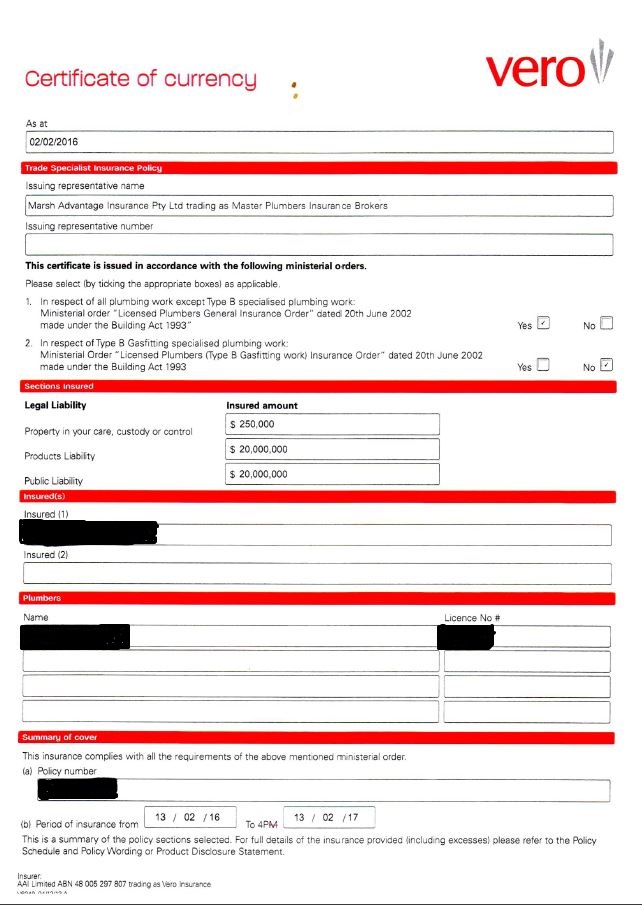

Therefore, we would suggest that as a savvy consumer considering engaging the services of any licenced Victorian plumber to carry out works at your property, that you are Well Within Your Rights to ask for a photocopy of the plumber’s Insurance Certificate of Currency that covers the time period for the works. This document will clearly identify the policy number and the period of insurance, along with the amount of insurance and the identity of the Insurer. This, combined with the Certificate of Compliance, is then your guarantee of protection.

We recommend that once you have a copy, the plumber’s Certificate of Currency should be placed in safe keeping just in case you ever need it. Don’t forget the warranty lasts at least 6 years and potentially up to 10 years.

If the worst happens and the work is defective and/or it causes damage to your property and the plumber will not or cannot make good the situation, then you already know who the insurer is and don’t have to battle the FOI curtain at the VBA. That means you can make your claim immediately on the insurer.

If your primary contract is with a Builder, then we recommend that you should make the request for the plumber’s Certificate of Currency through them.

Of course and ideally, a consumer will be able to work with their licenced plumber to arrange for them to return to the site and make good any minor problems however if major issues arise and/or there is a breakdown in the working relationship and/or if the plumber goes AWOL or there is a major disaster of some sort – then the insurance details will be invaluable.

Be aware that if defective plumbing work causes damage to your house e.g the plumbing work floods out the property, any claim you make on your House & Contents insurance policy will normally be denied because there’s an exclusion for those sorts of claims.

The Ministerial Order which regulates the insurance industry for licenced plumbers makes provision for a third party to make a claim against a plumber’s policy if defects in the works exist or if consequential losses have been incurred.

According to the Building Act 1993, before even starting the job plumbers need to supply you up front with details of how the insurance system works – for more information see:

http://www.vba.vic.gov.au/__data/assets/pdf_file/0020/26390/Insurance-on-plumbing-work.pdf

A plumber can be fined for not giving you this insurance information. In our experience though, it rarely if ever happens in real life and once a claim situation results, it’s normally very difficult for a consumer to navigate their way through the VBA complaints process, the VBA investigation process, the VBA FOI application process and then finally identify the insurer involved. You could be looking at a year before you even know who the insurer is.

If a plumber intends to carry out works at your site in a compliant manner which is in accordance with the current regulations and utilise quality materials with adequate supervision of employees then surely they should have no reason to take umbrage at your request for a copy of their currency certificate!

It’s very strange that when entering into a Major Domestic Building Contract where there is Domestic Builders Warranty involved, a licenced builder is legally required to provide you with their full insurance details up front but no such requirement exist on plumbers no matter how large the project.

You are the consumer and you are Well Within Your Rights to protect your own interests here, so next time you are thinking about getting work done by a plumber, ask for a copy of their insurance currency certificate up front. If they refuse, you don’t want to deal with them anyway and should just walk away.

A sample Certificate of Currency for a plumber is below. Just remember there are at least half a dozen insurance companies who underwrite this business in Victoria, so the format and look of the certificate might be different, but what you need to find at the very least is the name of the insurer, the insurance policy number plus a start date and an expiry date for the policy. Also make sure it refers to the policy being issued pursuant to the provisions of the Licenced Plumbers General Insurance Order 2002.

Sorry, the comment form is closed at this time.